|

||||||

| Applied

Econometrics

Econ 508 - Fall 2008 e-Tutorial 2: A Brief Introduction to R |

||||||

| Welcome

to e-Tutorial, your on-line help to Econ508. The introductory material

presented below is the second of a series of handouts that will be

distributed along the course, designed to enhance your understanding of

the topics and your performance on the problem sets. The present issue

focuses on the basic operations of R. The core material was extracted from

Douglas Simpson's "Computational Statistics" (2001) course, and

Gregory Kordas' Econ472 (1999) class notes. The usual disclaimers

apply.

What's

R?

Accessing

R

Installing

R (Windows Version)

Useful Links

Downloading

Data

Example

- The U.S. Economy in the 1990s

To download

the data, please follow the general steps below:

US90<-read.csv("C:/Econ472/US90.csv",

header=T)

Save the file

as US90code.txt. This will create a routine to download the data.

Here you are naming the data set as "US90" and asking R to import it from

the file "US90.csv" located in the directory "C:/Econ508/". The term "header"

refers to the names of the variables in the first row. The lines 2-9 corresponds

to each individual variable - in order to work with them, you need to extract

them from the data frame (single object) and give respective names after

that (multiple objects).

f) Start R

(i.e., run RGui.exe). In the toolbar, go to "File", "Source R code", and

open the file US90code.txt containing your routine. (Be careful to

name the right directory where you have saved your routine.)

g) In the window called R Console, type US90. You will be able to see the matrix containing the data (a.k.a. data frame). If you type the name of a single variable, you will be able to visualize that on the screen as a vector. Now you are ready to work with your data!! Basic Operations

If you also

wish to know the standard deviation of the series, type

If you are

only interested in a single variable, just include its name after the command

If you are

in interested only in subset of your data, you can inspect it using filters.

For example, begin by checking the dimension of the data matrix:

This means

that your data matrix contains 11 rows (corresponding to the years 1992

to 2002) and 8 columns (corresponding to the variables). If you are only

interested in a subset of the time periods (e.g., the years of the Clinton

administration), you can select it as a new object:

and then compute

its main statistics:

If you are

only interested in a subset of the variables (e.g., consumption and investment

growth rates), you can select them by typing:

and then compute

its main statistics:

To create new variables, you can use traditional operators (+,-,*,/,^) and name new variables as follows: add or

subtract: lagyear<-year-1

Last, but

not least, the Help command (e.g., type help("log") in the R Console) contains

short but useful information on the main packages with functions provided

by R. Later in Econ508, you will learn how to create your own functions

in R.

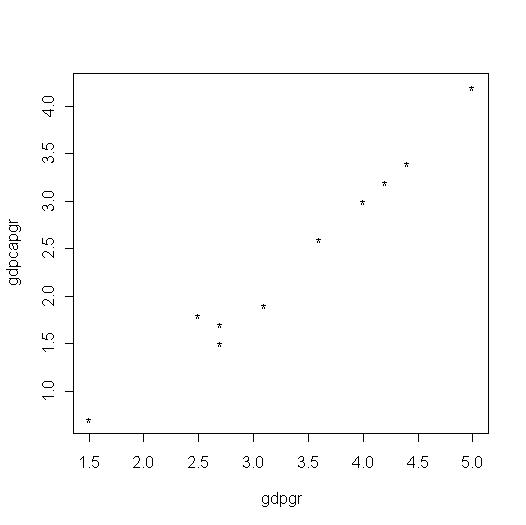

Exploring Graphical Resources Suppose now

you want to check the relationship among variables. For example, suppose

you would like to see how much GDP growth is related with GDP per capita

growth. This corresponds to a single graph that could be obtained as follows:

And the result

will be:

Another useful

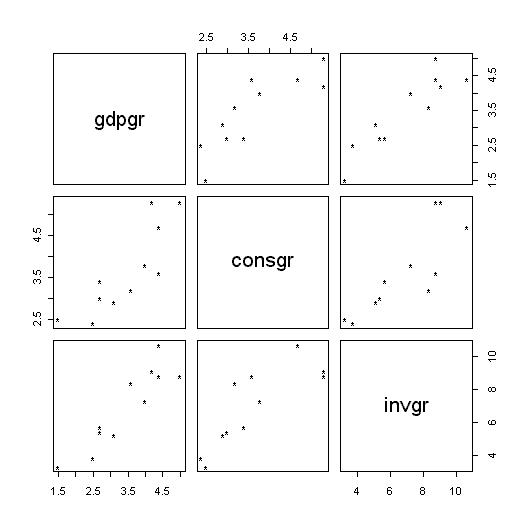

tool is the check on multiple graphs in a single window. For example, suppose

you would like to expand your selection, and check the pair wise

relationship of GDP, Consumption, and Investment Growth. You can obtain

that as follows:

The result will be:

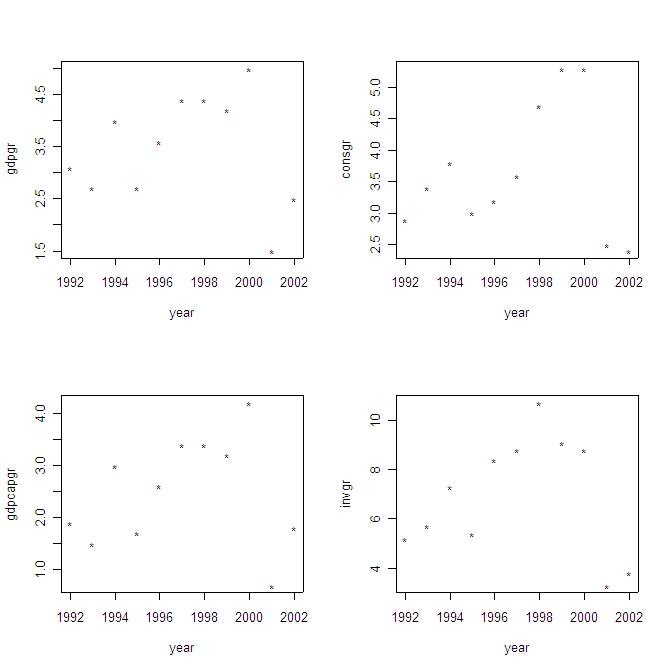

Suppose you would like to see the performance of multiple variables (e.g., GDP, GDP per capita, Consumption, and Investment growth rates) along time. The simplest way is as follows: par(mfrow=c(2,2))

Here the command "par(mfrow=c(2,2))" creates a matrix with 2 rows and 2 columns in which the individual graphs will be stored, while the command "plot" is in charge of producing individual graphs for each selected variable. The output will be:

You can easily

expand the list of variables to obtain a graphical assessment of the performance

of each of them along time. You can also use the graphs to assess cross-correlations

(in a pair wise sense) among variables.

Linear Regression Before running

a regression, it is recommended you check the cross-correlations among

covariates. You can do that graphically (see above) or using the following

simple command:

The output will be: > c1

From the matrix above you can see, for example, that GDP and GDP per capita growth rates are closely related, but each of them has a different degree of connection with unemployment rates (in fact, GDP per capita presents higher correlation with unemployment rates than total GDP). Inflation and unemployment present a reasonable degree of positive correlation (about 36%). Now you start

with simple linear regressions. For example, let's check the regression

of GDP versus investment growth rates. You just type:

And the output will be: Call:

Residuals:

Coefficients:

Residual

standard error: 0.4599 on 9 degrees of freedom

Please note that you don't need to include the intercept, because R automatically includes it. In the output above you have the main regression diagnostics (F-test, adjusted R-squared, t-statistics, sample size, etc.). The same rule apply to multiple linear regressions. For example, suppose you want to find the main sources of GDP growth. The command is: model2<-lm(gdpgr~consgr+invgr+producgr+unemp+inf)

And the output is: Call:

Residuals:

Coefficients:

Residual standard

error: 0.517 on 5 degrees of freedom

In the example above, despite we have a high adjusted R-squared, most of the covariates are not significant at 5% level (actually, only investment is significant in this context). There may be many problems in the regression above. During the Econ508 classes, you will learn how to solve those problems, and how to select the best specification for your model. You can also

run log-linear regressions. To do so, you type:

And the output will be: Call:

Residuals:

Coefficients:

Residual

standard error: 0.1729 on 5 degrees of freedom

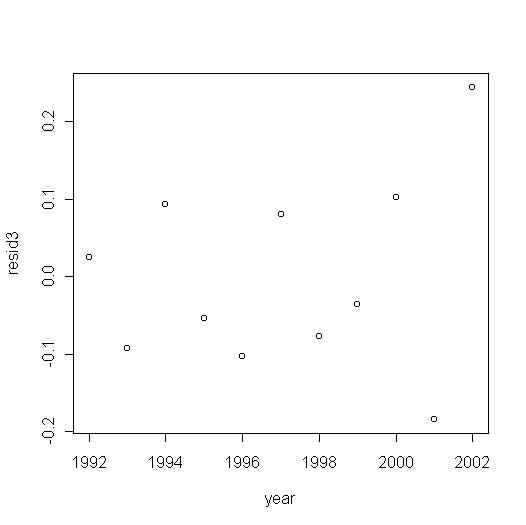

Finally, you

can plot the vector of residuals as follows:

The output will be:

You can also

obtain the fitted values and different plots as follows:

Linear Hypothesis Testing Suppose you

want to check whether the variables investment, consumption, and productivity

growth matter to GDP growth. In this context, you want to test if those

variables matter simultaneously. The best way to check that in R is as

follows. First, run a unrestricted model with all variables:

Then run a

restricted model, discarding the variables under test:

Now you will

run a F-test comparing the unrestricted to the restricted model. To do

that, you will need to write the F-test function in R, as follows:

(The theory comes from Johston and DiNardo (1997), p. 95, while the R code

is a version of Greg Kordas' S code. I've adjusted it for this specific

problem.)

F.test<-function(u,r)

After that,

you can run the test and obtain the F-statistic and p-value:

$Fprob

And the conclusion

is that you can reject the null hypothesis of joint non-significance at

1.13% level.

Saving Operations in R The simplest

way to save commands in R is through the use of a routine. For example,

you can append your original routine US90code.txt with the commands you

have typed in the R console during the last session. Next time you open

this routine, all operations will be registered, and you can access previous

outputs by calling the objects you've created.

|

||||||