| Welcome

to the first issue of e-Tutorial, the on-line help to Econ 508. The introductory

material presented below is the first of a series of handouts that will

be distributed along the course, designed to enhance your understanding

of the topics and your performance on the homework. This very first

issue focuses on the basic operations of the main software used in the

course (STATA). The core material was extracted from Gregory Kordas' "Computing

in Econ 472" (1999) and "A Tutorial in Stata" (1999). The usual

disclaimers apply.

Accessing

Stata

The statistical

package Stata can be found at the OCSS (Office of Computing and Communications

for Social Sciences) lab, located at the 212 Lincoln Hall. Also, you can find Stata at the Foreign Languages Building (FLB) (room G8). It is also available

at the Econometrics Lab, DKH, for students enrolled in the Econometrics

field or other classes that require lab experiments.

STATA has

an extraordinary set of reference books, and by this reason some students

may be interested in purchasing the package. In those cases, the best strategy

is to form a group of students and make a special order to STATA Inc. For

Econ 508 purposes, however, the weekly edition of e-Tutorial will bring

all necessary information to solve the homework.

Downloading

Data

The first

step required to solve the homework is to download the respective data

sets. Usually the data will be posted in the ASCII or text formats.

In order to work with the data, I suggest the following steps:

a) Go to

the web page containing the data, and save it in a floppy disk or a hard

drive. If the latter is chosen, I suggest you create a directory exclusively

dedicated to Econ508 materials.

b) After

saving, go to STATA and infile the data in its original format.

c) Finally,

save the data in the format .dta, adopted by STATA.

Example

- The U.S. Economy in the 1990s

Let's start

with an analysis of the performance of the U.S. economy during the 1990s.

I have collected annual data on GDP growth, GDP per capita growth, private

consumption growth, investment growth, manufacturing labor productivity

growth, unemployment rate, and inflation rate. The first two variables

can be seen as dependent variables, and you should test whether they are

close substitutes or the population size has dramatically changed during

this period. Consumption, investment, and productivity can be seen as factors

that enhance GDP growth, and therefore you should expect positive covariates

for those variables. Finally, unemployment and inflation rates are intrinsically

correlated, and you should check whether any (or both) can be included

in our simplistic growth model.

Please click

here

to access the data in a text format. After data, save as recommended, and

go to the Stata Command window. There, please type the following command:

infile

year gdpgr consgr invgr unemp gdpcapgr inf producgr using "a:\US90.txt"

(I assumed

that you have saved the data set in a floppy disk and the file has .txt

extension. If the file has a .raw format or you wish to save it in a different

location, just repeat the command above doing the respective adjustments

(i.e., including your preferred directory and changing file extension).

For ASCII data with .raw format, you can omit the extension. E.g.:

infile

year gdpgr consgr invgr unemp gdpcapgr inf producgr using "c:\Econ472\US90"

In the commands

above, the term "ïnfile" refers to the action executed by Stata, the

terms "gdpgr, ..., producgr" correspond to the name of the respective variables

according to the order they appear in the data set, and the rest of the

command describes the location you have chosen to save the downloaded data.

After that, you can visualize your data using the button "Data Editor"

in the toolbar. The final step is to save the file in a Stata format, with

the extension .dta. Now you are ready to work with your data!!

Basic Operations

A useful

way to explore your data is checking the main statistics of each variable.

For example, in the Stata Command window you can obtain the minimum, maximum,

arithmetic mean, and standard deviation of each variable in your data set

by typing

summarize

Variable

| Obs

Mean Std. Dev. Min

Max

---------+-----------------------------------------------------

year | 11

1997 3.316625 1992

2002

gdpgr | 11 3.463636

1.050974 1.5

5

consgr | 11 3.645455

1.03476 2.4

5.3

invgr | 11 6.954545

2.408885 3.3

10.7

unemp | 11 5.327273

1.125247 4

7.5

gdpcapgr

| 11 2.490909

1.048289 .7

4.2

inf | 11 2.590909

.5204893 1.5

3.4

producgr

| 11 4.309091

1.590883 1.9

7.2

If you also

wish to know the behavior along the percentiles, type

summarize,

detail

If you are

only interested in a single variable, just include its name after the command

summarize

gdpgr, detail

If you are

only interested in a subset of your data, you can inspect it using filters.

E.g., if you are only interested in the years of the Clinton administration,

you type

summarize

if year>=1993 & year<=2000

And then you

can contrast that period with the family Bush administrations

summarize

if year<1993 | year>2000

You may also

check all years but the election years, to avoid political cycles:

summarize

if year~= 2000 & year~=1996 & year~=1992

At this point

you have already noticed the main logical operators in Stata:

>=

means "greater or equal",

<=

means "less or equal",

&

means "and",

|

means "or".

The arithmetic

operators are as usual (+, -, *, /). And to create a new variable

using them, you can do as follows: Suppose you wish to know how close the

GDP growth is to the GDP per capita growth. So, you create a ratio of those

two variables, and check it:

generate

gdpratio= gdpgr/ gdpcapgr

summarize

gdpratio, detail

The same procedure

can be done to obtain traditional transformations, such as

squares:

gen produc2=producgr^2

square

roots: gen infroot=sqrt(inf)

exponential:

gen expgdpgr=exp(gdpgr)

natural

logs: gen logunemp=log(unemp) or simply

gen lnunemp=ln(unemp)

base 10

logs: gen log10inf=log10(inf)

A final remark

is that you should choose a name for the generated variable with at most

8 characters, otherwise the system will give an error message. Nevertheless,

you can always describe your variables in more details using the commands

label or notes. Last, but not least, the Help toolbar contains short but

useful information on the main commands. It does not hurt visit it once

in a while...

Exploring

Graphical Resources

Suppose now

you want to check the relationship among variables. For example, you want

to see how much consumption and investment are correlated with GDP (all

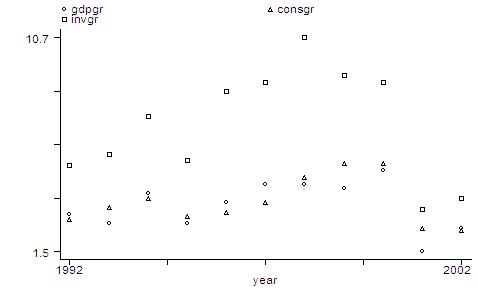

variables in growth rates). The command for that is:

graph

gdpgr consgr invgr year

The output

is a scatter of points for each series, with the investment series being

relatively higher than the other two series. If you are more interested

on the dynamics of the series than in the levels, you can re-scale the

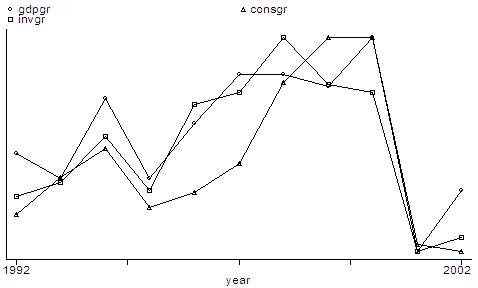

graph and connect the points. The command is as follows:

graph

gdpgr consgr invgr year, rescale c(lll)

In the command

above, "rescale" allows the shift on the series, and "c(lll)" connects

the points using lines for each series. Many other graph types are available

in STATA, and you can explore them as necessary. In this brief intro, the

following commands will be useful:

* to extract

the symbols on the series:

graph

gdpgr consgr invgr year, rescale c(lll) symbol(iii)

* to give

a title to the graph:

graph

gdpgr consgr invgr year, c(lll) b1(Figure 1. GDP, Consumption and Investment)

b2(year) l2(growth rate)

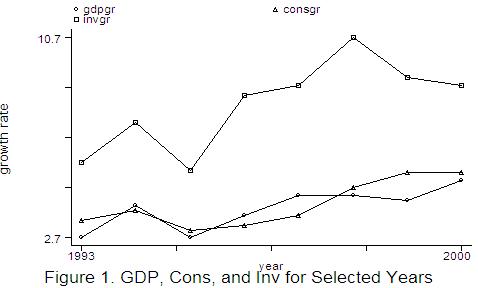

* to plot

only specific ranges:

graph

gdpgr consgr invgr year if year>=1993 & year<=2000, c(lll) b1(Figure

1. GDP, Cons, and Inv for Selected Years) b2(year) l2(growth rate)

Finally, you

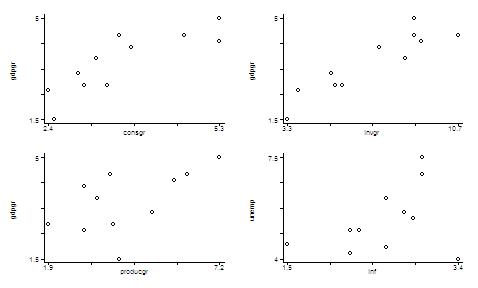

can combine graphs in a single figure. For example, suppose you would like

to obtain a graphical diagnostic on the relationship between GDP and consumption

growth rates, GDP and investment growth rates, GDP and productivity growth

rates, and revisit the relation between unemployment and inflation rates.

The commands to do that are as follows:

graph

gdpgr consgr, saving(part1)

graph

gdpgr invgr, saving(part2)

graph

gdpgr producgr, saving(part3)

graph

unemp inf, saving(part4)

graph

using part1 part2 part3 part4, margin(10)

Through the

commands above, you generated and saved four individual graphs, and plotted

them into a single figure. The command margin(10) means that you

are requiring a space between each pair of graphs about 10% of the whole

picture. This is indeed a very useful tool to check pair wise correlation

among variables, before you run a regression.

Linear

Regression

As remarked

above, before running a regression, it is recommended to check the cross

correlation among covariates. You can do that graphically (see above) or

using the following simple command:

correlate

gdpgr gdpcapgr consgr invgr producgr unemp inf

(obs=11)

| gdpgr gdpcapgr consgr

invgr producgr unemp inf

---------+---------------------------------------------------------------

gdpgr | 1.0000

gdpcapgr

| 0.9890 1.0000

consgr | 0.8394 0.8347 1.0000

invgr | 0.9097 0.8841 0.8270

1.0000

producgr

| 0.5708 0.6003 0.7050

0.5238 1.0000

unemp | -0.3035 -0.4143 -0.4761 -0.3684 -0.5336

1.0000

inf | -0.1012 -0.1230 -0.1198 -0.3090 -0.0832

0.3590 1.0000

From the matrix

above you can see, for example, that GDP and GDP per capita growth rates

are closely related, but each of them has a different degree of connection

with unemployment rates. In fact, GDP per capita growth rates present higher

negative correlation with unemployment rates (41.43%) than total GDP growth

rates do (30.35%). Inflation and unemployment rates present a reasonable

degree of positive correlation (35.90%).

Now you start

with simple linear regressions. For example, let's check the individual

regressions of GDP with consumption and investment growth rates:

regress

gdpgr consgr

regress

gdpgr invgr

The output

will be

.

regress gdpgr consgr

Source | SS

df MS

Number of obs = 11

---------+------------------------------

F( 1, 9) = 21.46

Model | 7.78197201 1 7.78197201

Prob > F = 0.0012

Residual

| 3.26348251 9 .362609168

R-squared = 0.7045

---------+------------------------------

Adj R-squared = 0.6717

Total | 11.0454545 10 1.10454545

Root MSE = .60217

------------------------------------------------------------------------------

gdpgr | Coef. Std. Err.

t P>|t| [95%

Conf. Interval]

---------+--------------------------------------------------------------------

consgr | .8525216 .1840263

4.633 0.001 .4362251

1.268818

_cons | .3558076 .6949943

0.512 0.621 -1.216379

1.927994

------------------------------------------------------------------------------

.

regress gdpgr invgr

Source | SS

df MS

Number of obs = 11

---------+------------------------------

F( 1, 9) = 43.22

Model | 9.14164404 1 9.14164404

Prob > F = 0.0001

Residual

| 1.90381048 9 .211534498

R-squared = 0.8276

---------+------------------------------

Adj R-squared = 0.8085

Total | 11.0454545 10 1.10454545

Root MSE = .45993

------------------------------------------------------------------------------

gdpgr | Coef. Std. Err.

t P>|t| [95%

Conf. Interval]

---------+--------------------------------------------------------------------

invgr | .3969137 .0603774

6.574 0.000 .2603305

.5334969

_cons | .7032821 .4422039

1.590 0.146 -.2970526

1.703617

------------------------------------------------------------------------------

Please note

that you don't need to include the intercept, because STATA automatically

includes it. In the output above you have the main regression diagnostics

(ANOVA, adjusted R-squared, t-statistics, sample size, etc.). The same

rule apply to multiple linear regressions. For example, suppose you want

to find the main sources of GDP growth. You type:

regress

gdpgr consgr invgr producgr unemp inf

And the output

will be:

.

regress gdpgr consgr invgr producgr unemp

inf

Source | SS

df MS

Number of obs = 11

---------+------------------------------

F( 5, 5) = 7.27

Model | 9.70924721 5 1.94184944

Prob > F = 0.0242

Residual

| 1.33620731 5 .267241462

R-squared = 0.8790

---------+------------------------------

Adj R-squared = 0.7581

Total | 11.0454545 10 1.10454545

Root MSE = .51695

------------------------------------------------------------------------------

gdpgr | Coef. Std. Err.

t P>|t| [95%

Conf. Interval]

---------+--------------------------------------------------------------------

consgr | .1822094 .3605194

0.505 0.635 -.7445351

1.108954

invgr | .3448859 .1338048

2.578 0.050 .0009296

.6888422

producgr

| .0490201 .1547288

0.317 0.764 -.3487228

.4467631

unemp | .0551669 .1897954

0.291 0.783 -.4327176

.5430514

inf | .3019558 .372596

0.810 0.455 -.6558326

1.259744

_cons | -.8865854 1.492931 -0.594

0.578 -4.724287 2.951116

------------------------------------------------------------------------------

In the example

above, despite we have a high adjusted R-squared, most of the covariates

are not significant at 5% level (actually, only the investments coefficient

is significant at this level). There may be many problems in the regression

above. On the Econ 508 classes you will learn how to solve most of those

problems, including how to select the best specification for a model.

You can also

run a log-linear regression after transforming each variable into a natural

log scale. To do so, you type:

gen

lngdpgr=ln(gdpgr)

gen

lnconsgr=ln(consgr)

gen

lninvgr=ln(invgr)

gen

lnproduc=ln(producgr)

gen

lnunemp=ln(unemp)

gen

lninf=ln(inf)

regress

lngdpgr lnconsgr lninvgr lnproduc lnunemp lninf

Source | SS

df MS

Number of obs = 11

---------+------------------------------

F( 5, 5) = 7.19

Model | 1.07467131 5 .214934262

Prob > F = 0.0247

Residual

| .149400242 5 .029880048

R-squared = 0.8779

---------+------------------------------

Adj R-squared = 0.7559

Total | 1.22407155 10 .122407155

Root MSE = .17286

------------------------------------------------------------------------------

lngdpgr

| Coef. Std. Err.

t P>|t| [95%

Conf. Interval]

---------+--------------------------------------------------------------------

lnconsgr

| .114882 .4666926

0.246 0.815 -1.08479

1.314554

lninvgr

| .779761 .3081229

2.531 0.052 -.0122942

1.571816

lnproduc

| .0950277 .1935535

0.491 0.644 -.4025174

.5925728

lnunemp

| .2009322 .3716735

0.541 0.612 -.7544849

1.156349

lninf | .1184624 .2785439

0.425 0.688 -.5975574

.8344822

_cons | -.9912522 .787582

-1.259 0.264 -3.015796

1.033292

------------------------------------------------------------------------------

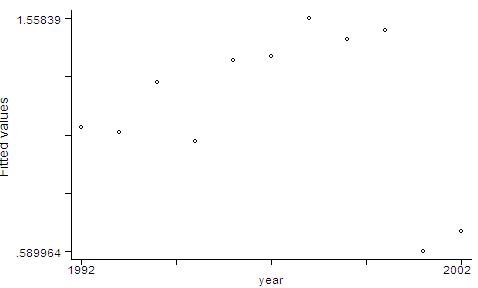

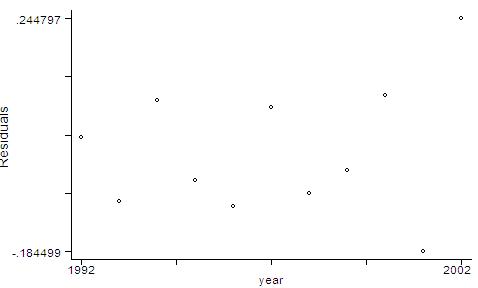

Finally, you

can generate predicted values of the dependent variable and of the residuals,

and plot them:

predict

lngdpfit

graph

lngdpfit year

predict

lngdpres, resid

graph

lngdpres year

Linear

Hypothesis Testing

After running

the regressions above, we can proceed with tests of linear hypothesis on

the covariates. For example, suppose you would like to be sure that investment

growth "matters" to GDP growth. **(Please recall that you are no longer

performing causality tests, but only detecting whether the two variables

are correlated. Through the Econ 508 classes, you will learn how to perform

causality tests.)** Thus, you proceed with:

test

lninvgr

And the output

will be:

(

1) lninvgr = 0.0

F( 1, 5) = 6.40

Prob > F = 0.0525

You just performed

a F-test for the null hypothesis of lninvgr=0 against the alternative of

lninvgr ~= 0. The computed F-statistic is the squared of the popular t-statistic.

The result means that investment growth rates (in logs) are significantly

different than zero at 5.25% level, and therefore they contribute

to explain the variation in GDP growth rates (in logs).

To test the

joint significance of two or more covariates, you type:

test

lninvgr lnconsgr lnproduc

And the output

will be:

(

1) lninvgr = 0.0

(

2) lnconsgr = 0.0

(

3) lnproduc = 0.0

F( 3, 5) = 11.40

Prob > F = 0.0113

Here you

are testing the null hypothesis that all covariates are zero against the

alternative hypothesis that at least one of them is different than zero.

The result shows that we cannot accept the null at 1.13% of significance,

i.e., some of them are significantly different than zero at this level.

So, some of them "matter" in explaining the variation in GDP growth rates

(logs) along the years.

You could

also extend your tests and check the equality of covariates. For example,

suppose you would like to know if investments and consumption have similar

coefficients:

test

lninvgr=lnconsgr

The output

will be:

(

1) - lnconsgr + lninvgr = 0.0

F( 1, 5) = 0.79

Prob > F = 0.4143

This is similar

to test whether their difference is zero (null hypothesis) or different

than zero (alternative). The conclusion is that, at 5% significance level,

we cannot reject the null hypothesis of similarity.

|