|

||||||

| Applied

Econometrics

- Fall 2004

Lecture 8 Figure 1: R code |

||||||

|

#Edit the function predict.arima0 substituting

the following two lines:

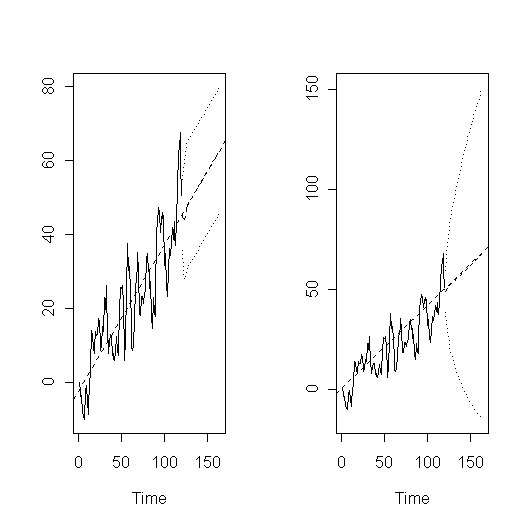

# Figures to illustrate the difference between forecasting in Trend

dev.off()

|

||||||

|

||||||

| Applied

Econometrics

- Fall 2004

Lecture 8 Figure 1: R code |

||||||

|

#Edit the function predict.arima0 substituting

the following two lines:

# Figures to illustrate the difference between forecasting in Trend

dev.off()

|

||||||

| Last update: September 30, 2004 . Send comments to: lamarche@uiuc.edu |